If you would like purchase a house, however you don’t have a lot of discounts or a reduced credit rating, you might be interested in exactly what a keen FHA loan must promote. Brand new Federal Houses Management, a division of Us Institution regarding Construction and you can Metropolitan Advancement (HUD), assures FHA mortgage brokers to own first-time people and people having reduced-than-better finances. These types of fund want the very least down payment of just step 3.5% and you may a credit score out-of simply 580. You may qualify when your rating can be as reduced due to the fact five-hundred, provided that you devote down about ten%.

You have read you to definitely FHA home loan standards become more strict than just conventional loans, but it get shock one to understand just how flexible their houses choices are. We have found a close look within sort of belongings you can buy with an enthusiastic FHA mortgage and exactly what you are going to end a home out-of are FHA-recognized.

You can use a keen FHA mortgage to order a variety of property types. Whenever you are single-family home will be the most common, he or she is away from your own sole option. Here are the other sorts of property that are eligible for FHA loans.

Are formulated Homes

A manufactured residence is a manufacturer-founded house one to will come on-site totally constructed and ready to end up being installed. Our home is meant to be went immediately after, hence is different from a mobile house that may be moved multiple minutes if required.

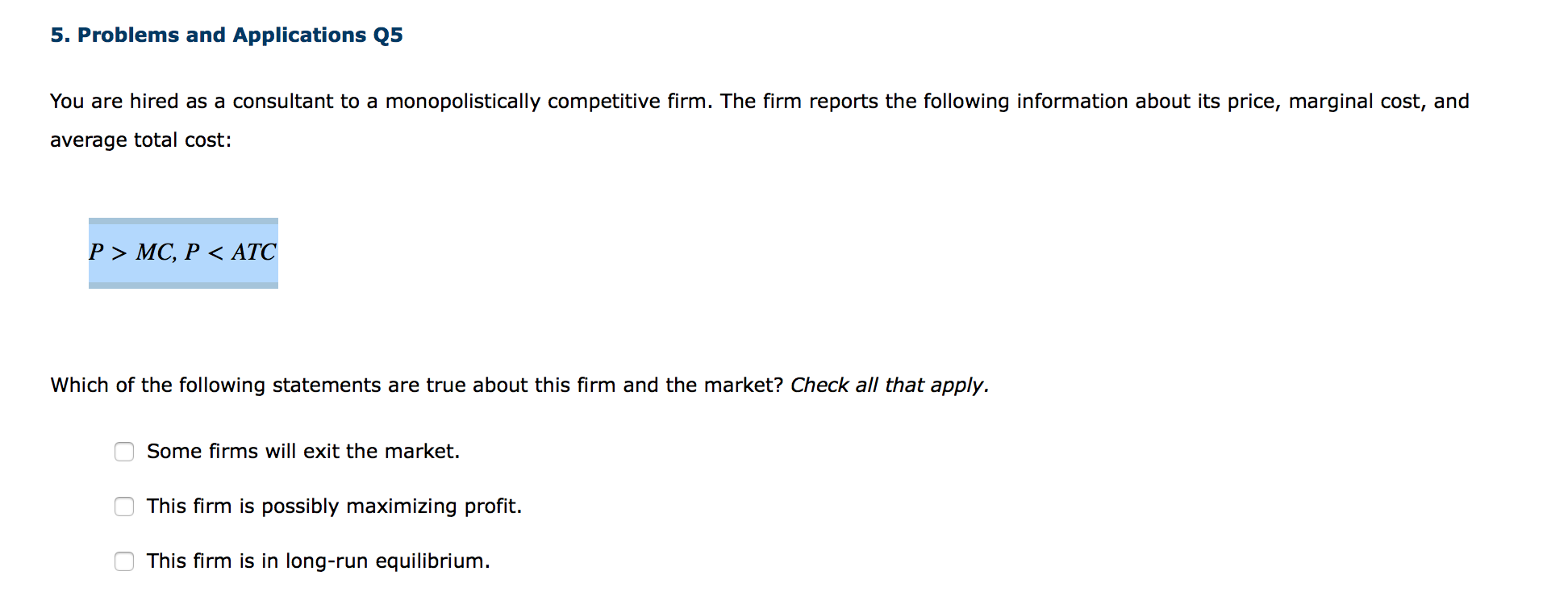

FHA are created home loans need a slightly higher credit rating than other FHA-acknowledged characteristics. Qualified homes must be constructed on or just after June fifteen, 1976, and see local and you may state guidelines. Minimum square video footage requirements may also implement, and family should be installed on a long-term foundation.

Fixer-Uppers

Incapacity to meet up lowest assets conditions you will definitely disqualify an effective fixer-higher away from a standard FHA financing. Although not, in case your domestic we should get demands big renovations, you could get an FHA 203(k) treatment mortgage. Remember that the house need still see very first architectural and you will energy savings criteria to help you meet the requirements.

A keen FHA 203(k) mortgage makes you pick and redesign your house you desire. Additionally, it is offered while the a refinance mortgage on the domestic your currently live in. After you’ve completed the desired fixes, an enthusiastic appraiser commonly reevaluate the brand new residence’s viability to make sure they suits minimal assets requirements.

Mixed-Play with Characteristics

Although you can’t buy a residential property with an enthusiastic FHA loan, a blended-use possessions may be qualified for as long as it is mainly zoned domestic while decide to explore at least 51% from it as your first household. The rest of the home can be used for almost every other aim, eg renting it out to create extra money.

Multifamily Housing

Particular duplexes and you can condominium houses with up to four tools is qualified to receive FHA funds. Glance at HUD’s variety of approved programs to find out if the home we would like to pick keeps found brand new FHA’s minimum possessions eligibility conditions.

To buy a condo strengthening can be your chance to generate more cash from the leasing away the main assets. Just be aware you ought to live in one of brand new products you purchase towards the building as FHA-recognized. Other book requirements plus apply to FHA condominium funds.

The next Home

FHA funds usually are regarded as basic-go out homebuyer financing, but you may be eligible to buy one minute FHA-insured home beneath the best items. The certificates, in depth in HUD 4000.1, through the following the:

- Your task demands you to move in.

- The home no further match your family’s means.

- The borrowed funds-to-really worth ratio on the latest house is 75% otherwise smaller.

- You co-finalized an FHA loan to have a home that you don’t inhabit.

- You have divorced no expanded live in the FHA-covered domestic.

As to the reasons a house Might not be FHA-Recognized

Since there is a great deal more leniency having FHA finance than you may enjoys knew, certain limits however implement. Here are the popular scenarios one disqualify a home to have an FHA mortgage.

Trips Belongings and you can Money Features

You can just use an enthusiastic FHA mortgage to order a home you plan to use as your pri is intended to prompt primary homeownership. If you’d like to pick a secondary house otherwise money spent, you’ll want to below are a few other types of lenders.

Little Land

New affordability and you may portability out-of small property cause them to an increasing pattern within the nation. Sadly, characteristics are only entitled to a keen FHA financing if they’re attached so you can a long-term basis. This really is a condition of your financing just like the homes to your tires aren’t categorized because the a home, as well as characteristics bought that have an FHA mortgage have to be categorized as such.

Failure to satisfy FHA Minimum Assets Requirements

FHA funds enjoys even more defense, shelter, and you can soundness criteria, that will stop you from getting the house you want. It protects the financial institution if the debtor defaults with the loan, as well as the domestic goes in foreclosures. Additionally, it protects the latest debtor off unanticipated domestic resolve debts and you will repairs costs.

FHA monitors payday advance loans Maine tend to disqualify belongings which aren’t when you look at the best standing because they have large requirements than simply normal all about home inspections. Brand new degree recommendations change regularly, thus ask a keen inspector for more information just before if in case your house we would like to buy try FHA-acknowledged.

Submit an application for an FHA Mortgage Now

The fresh FHA mortgage program has many nuance to they. If you are looking getting specific answers regarding the qualifications, we advice conversing with a specialist loan administrator at Financial Principles Home loan. We are able to counsel you on your own eligibility that assist you see some of the reasonable rates for the FHA lenders regarding nation. To begin with, please call us at the (405) 722-5626 otherwise sign up for a home loan on the web.